How to Think About Taxes in Retirement

How to Think About Taxes in Retirement (It’s Not What Most People Expect)

When we think about retirement tax planning, most people assume their taxes will naturally be lower once they stop working. In reality, that’s often not true—especially for retirees who spent decades deferring income into a 401(k).

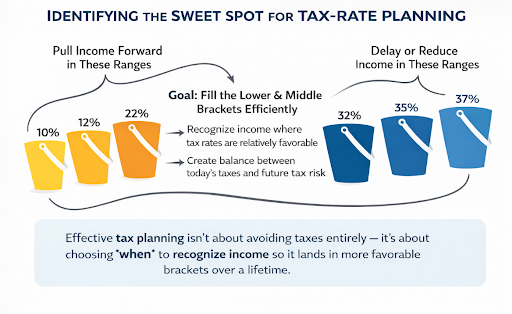

The image above illustrates a simple but powerful idea:

The goal isn’t to avoid taxes altogether—it’s to control when income shows up and which tax brackets it fills.

The Retirement Tax Trap: Too Much Deferred Income

If you’ve consistently contributed to a traditional 401(k) over a 30–40 year career and allowed it to compound, you may walk into retirement with a large pre-tax balance. Once Required Minimum Distributions (RMDs) begin, that income becomes unavoidable.

Now layer on other income sources.

I see this frequently when working with New York State teachers who are eligible for:

A NYS pension

Social Security benefits

Many of these retirees earn the same—or even more—after retiring than they did while working. Add RMDs on top of pension and Social Security income, and taxable income can land squarely in the 32%, 35%, or even higher brackets.

At that point, the long-term tax deferral that felt smart during your working years can turn into a tax problem in retirement.

Why “Tax-Deferred at All Costs” Isn’t Always Optimal

The traditional advice—maximize pre-tax contributions while working—ignores one critical variable: future tax rates.

Federal tax rates today are historically low.

About 20 years ago, the top federal marginal rate was 39.6%

Today, the top rate is 37%, with lower brackets also compressed

At the same time, the federal deficit continues to grow, making higher future tax rates a very real risk. Deferring income into an unknown (and potentially higher) tax environment isn’t always the best trade-off.

Why Roth Accounts Matter More Than Ever

Roth assets give retirees flexibility that traditional retirement accounts simply don’t:

No RMDs during your lifetime

No forced income spikes later in retirement

Tax-free growth and withdrawals

Better outcomes for beneficiaries

For many households, Roth IRA contributions, Roth 401(k) contributions, or proactive Roth conversions can help “fill” lower and middle tax brackets intentionally—before RMDs begin.

Coordinating Income Sources Strategically

Effective retirement tax planning often involves mixing income sources, such as:

Partial Roth conversions in lower-income years

Taxable account withdrawals before tapping tax-deferred accounts

72(t) distributions for those retiring before age 59½

Coordinating pension start dates and Social Security claiming strategies

The objective is simple:

Recognize income when tax rates are relatively favorable and avoid pushing yourself into higher brackets later.

The Big Picture

Retirement tax planning isn’t about chasing deductions—it’s about creating control.

If most of your wealth is tied up in tax-deferred accounts, you’ve deferred the problem, not solved it. A thoughtful strategy that incorporates Roth assets and proactive planning can reduce lifetime taxes, smooth income, and preserve more of what you’ve built.

If you’re approaching retirement—or already retired—and want to understand how your pension, Social Security, and retirement accounts interact from a tax perspective, that’s exactly where careful planning makes the biggest difference.